A meaningful reporting system is essential for successful, sustainable corporate governance.

It enables transparent and well-founded decisions based on figures, data and facts. A recent research project by the University of Pforzheim (ESG HR Barometer) comes to the conclusion, among other things, that 48 percent of the companies surveyed have not yet dealt with the topic or have done so for less than six months. 13 percent state that HR is not yet prepared for the challenges of ESG reporting requirement.

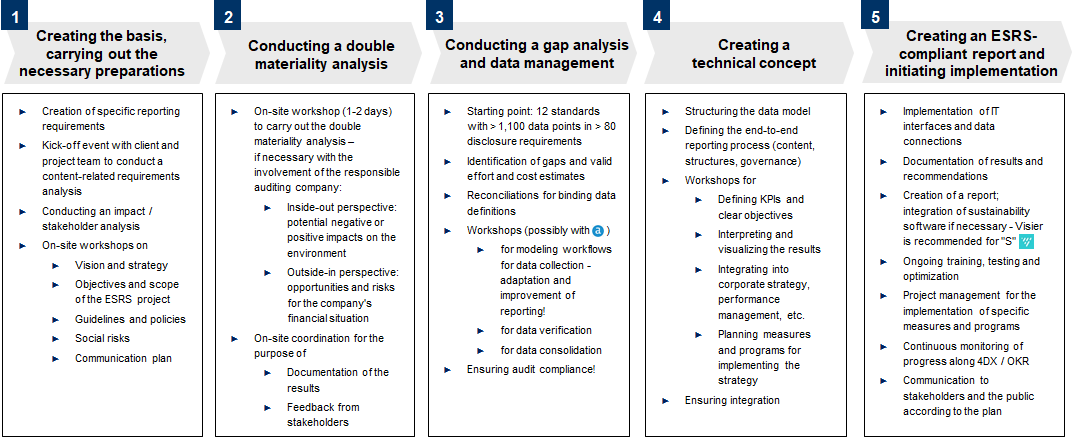

Many companies would like to have a kind of blueprint on which they can develop their sustainability report. This is critical in that the information to be reported depends on the results of the materiality analysis.

Implementation challenges

The following challenges must be addressed at an early stage in order to ensure successful ESRS reporting:

- The ESRS require companies to provide a large amount of non-financial information in the areas of environment, social and governance. Some of this data is to be collected for the first time.

- Companies may need to expand existing systems and implement new systems to be able to collect, consolidate and report the necessary data.

- Data collection is complex because companies have to consider not only their own organization, but also their upstream and downstream value chain.

Consequently, the IT infrastructure and the associated business processes play a central role in CSRD implementation with regards to data quality and efficiency. The required sustainability data is often distributed across different systems, departments and external partners.

A key task is to create an integrated data platform where all relevant information can be collected, standardized and analyzed. This not only facilitates reporting, but also creates the basis for a data-driven evaluation of corporate performance in the area of sustainability management.

Sustainability reporting in a nutshell

- Sustainability reporting integrates economic, ecological and social reporting. This means that accountability for the ecological and social impacts of business activities becomes a normal part of corporate reporting, alongside information on economic results.

- Companies subject to reporting requirements have to classify their economic activities as non-taxonomy-capable, taxonomy-capable or taxonomy-compliant.

- The Corporate Sustainability Reporting Directive (CSRD) is an amending directive. This means that the CSRD amends the existing accounting directive.

- The European Sustainability Reporting Standards (ESRS) ensure a consistent quality of sustainability reports. This means that the information contained therein is true, understandable, relevant, verifiable and comparable.

- The aim of sustainability reporting according to ESRS is to make clear the positive and negative impacts of a company’s business activities (impact materiality).

- At the same time, the risks and opportunities of these impacts must also be clear in the sustainability report (financial materiality).

- The relevant data points are derived from these IROs. These are pieces of information that specify the respective disclosure requirement. Such data points can be quantitative (number-based with absolute and relative key figures) or qualitative (descriptive).

- The sustainability report is usually included as a clearly identifiable part of the management report. ESRS 2 distinguishes between four reporting areas: corporate governance, strategy and business model, IROs, KPIs and objectives. ESRS 2 also defines four disclosure contents for the topic standards. In addition, the topic standards identified as material are part of the sustainability report.

Three specific services are in the foreground

The STRMgroup, in particular the business unit specializing in reporting and statistics, focuses on the following services in the area of sustainability:

- Creation and implementation of sustainability reports: This includes the integration of common standards into corporate strategy. In doing so, companies are supported in structuring reporting processes and collecting and processing the necessary data.

- Integration of key sustainability KPIs and reporting tools: With approaches such as the Sustainability Balanced Scorecard (SBSC), strategic sustainability goals can be made measurable and integrated into business processes. These scorecards help to transparently document the effectiveness of sustainability measures.

- Advice on reporting standards: Companies have to comply with various regulatory requirements. The STRIMgroup supports companies in understanding and implementing the requirements of the EU taxonomy and CSRD.

Digital solutions are integrated to automate and optimize data collection and evaluation for sustainability reports.

BDO proposes ten steps for the process of creating a structured sustainability report which are very suitable for an initial orientation (unfortunately only in German). The research project cited at the beginning suggests that many companies follow a two-stage process. In the first stage, the focus is on the regulatory requirements; in the second stage, the insights and interdependencies with regard to the 1.5-degree target that are possible on the basis of the reporting system.